THE FIRST SIGN OF CHANGE

..

Leonard Curtis as a company had been appointed as administrators, but under law there had to be named individuals who undertook the process. These were John Titley and Paul Reeves

County fans knowledge that the Club was totally out their hands came with the change of address to DTE House; Hollins Mount; Bury. This was done on 1st May and published by Companies House on 16th May.

..

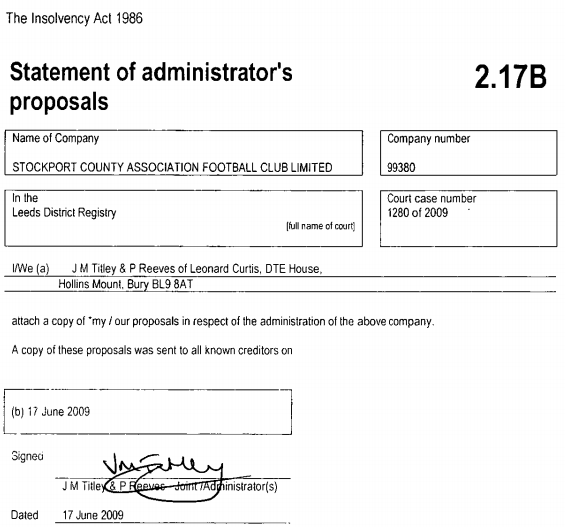

STATEMENT OF ADMINISTRATORS PROPOSALS

..

Published on 17th June was a 96 page report from Titley & Reeves. It looked at a whole series of issues – the background; the purpose of the administration and their proposals to achieve these. It also included a lost of information about the money owed; the liabilities, and to be fair gives a pretty good insight as to why it had happened.

..

THE PURPOSE OF THE ADMINISTRATION

..

The situation was described as follows:

..

The Club has a recent history of financial difficulties. The Club has struggled to fund a tax debt to HMRC which is estimated to be £630,000 and has been unable to repay a loan secured by the Debenture Holder for approximately £370,000. Following a substantial period of negotiations between the Debenture Holder and the Company without a solution, the Debenture Holder made the decision to file for the appointment of administrators over the Company and the Company entered administration on 30th April 2009.

..

The purposes of the administration are framed in law:

..

Rescuing the Company as a going concern; or

Achieving a better result for the Company’s creditors as a whole than would be likely if the Company were wound up; or

Realising assets in order to make a distribution to one or more secured or preferential creditors.

..

Putting things in English this put a range of options on the table. Making the Club profitable; or doing a deal with new owners; or winding things up and closing the Club down, whilst at the same time getting the best deal for the Creditors, (people and companies who were owed money by the Club)

..

CONSTRAINTS ON THE ADMINISTRATION

..

Reeves and Titley readily identified two major constraints:

1. The Golden Share. Any resolution of the administration which was to see the continuation of County, in the Football League, would require FA and FL approval, if the proposal was to create a new Company

2. The only assets which had a value were the players. And the first use of any transfer fees received would be paying off football creditors rather than using the cash to underpin the business. They prepared cash-flows which showed clearly that the the Club could not continue its operations without player sales. They concluded this part of their report by saying, “Other tangible assets ……. were insufficient to secure funding for continued trading”.

The madness of the deal that the Trust had done with Kennedy was laid bare. No assets and no revenue streams.

..

WHAT THE CLUB OWED AT THE POINT OF ADMINISTRATION – £7.4m!!!

..

Titley and Reeves included a schedule in their report which provided a wealth of detail about exactly what was owed. It was a staggering sum, amounting to £7.4m!! It was made up of a lot of different debts. The key ones were as follows:

David Farms Ltd – £370k: The amount which had accrued from the disastrous loan taken out by Beverley and Maguire, and which was the catalyst for administration

Cheshire Sports Ltd – £3.845m: This amount arose from the deal that the Trust did with Kennedy, under the guise of Cheshire Sports. The amount staggered me – I had long been a vociferous critic of the deal. I knew that it was unsustainable when first mooted, but never, ever, did I realise it was as bad as this!!

Football Creditors – £463k: This was cash owed to other clubs, largely for incoming transfers which were being paid ‘on the drip’. Under the rules any transfer fees received during the administration had to be used to meet these debts. The key ones were to Morecambe, (for Carl Baker); Crewe, (Owain fon Williams); Linfield, (Peter Thompson); Mansfield, (Johnny Mullins); Woodley Sports, (the sell-on element from Liam Dickinson’s move to Derby); and Nostell Miners Welfare, (Oli Johnson)

HM Revenues & Customs – £630k: This would have related to PAYE deducted from players and not yet paid together with VAT.

Employee Claims – £302k: One of the first acts of the administrators was to make a series of redundancies the most notable of which were Jim Gannon and Peter Ward. I never got my head around the fact that a Managers role could be ‘redundant’. The names may change but the role is a constant! Together with them were a whole raft of non playing employees, (FL rules prevented players from being included). This sum was the cost of the redundancies as defined by their contracts.

Directors Loans – £216k: There were a series of loans made by Directors.

Trade Creditors and Accruals – £922k; The schedule of amounts already owed, or becoming due in the near future, to companies, (many of which were local).

Shareholders – £500k: The amount that shareholders had put in and which was (nominally), repayable.

The only question was – how much cash, and the potential value of the assets, (in truth only the players), was actually in the business to pay these?

..

THE PALTRY AMOUNT AVAILABLE – £1.2m

..

Be under no illusion. The heading to this section suggests that there was £1.2m available to meet these debts, which of course still left an enormous black hole of £6.2m. Cash at the bank amounted to £224k, (largely as a result of the sterling work Martin Reid had done to drive cash into the business in March and early April). Some people criticised him for cancelling sell-on clauses in return for ready cash there and then at a significant discount, but it was done with the best of intentions.

Titley and Reeves had assessed how much cash they could get into the business – it provided, with hindsight, an interesting analysis. The book value, (ie the amount declared in the accounts); was totally irrelevant – it was simply a case of what people would pay.

They knew that they couldn’t undertake a fire sale of the whole squad – FL rule effectively prevented this, so they took advice from football agency WMG Management Europe Ltd as to the ‘saleable’ players for whom good money could be received. A value of £950k was arrived at and the first out of the door was Tommy Rowe, (£225k), for what was achievable at the time but would have, in normal circumstances, been a sale far too cheaply. Quite where the balance of £725k came from is a bit of a mystery. Players only have a transfer value if they are contracted – so I suppose that they were looking at names such as Carl Baker; Michael Raynes; Johnny Mullins and Paul Turnbull.

So with £225k cash and a player value of £950k that left a value of not much more than £25k for the rest of the Club. The Trust’s deal with Kennedy raises it head yet again. A business with no assets. Of course one must also recall the way in which Ekwood was stitched up by Kennedy, and the ground was separated from the Club.

Whatever the case, with a yawning chasm between £7.4m debts and only £1.2m assets any deal that was going to be struck would leave a lot of individuals and companies severely out of pocket, whether the Club continued in existence or not.

..

THE ADMINSTRATORS IMMEDIATE ACTIONS

..

As noted above the first few days after the season concluded at Brighton saw the redundancies of Gannon and Ward, (together with others), and the sale of Rowe. Expenditure had been cut and income generated. But this was only at about keeping the immediate wolf from the door.

The next step was to advertise the Club for sale, with a deadline for responses of 14th May, literally just a fortnight after the Club went into administration. The speed was needed in order to allow the transfer of the ‘Golden Share’ to new owners in advance of the new season.

Apparently a number of expressions of interest were received, but only two of them crystallised into bids. Both of them were conditional upon a deal with Kennedy for the use of EP, and also the transfer of the ‘Golden Share’ One of them fell at the first hurdle, (funding difficulties being proferred as the reason), but a second one led to an agreement with Titley and Reeves for the sale of the Club .

For a Club in such dire straits it looked, to me, to be an incredibly expensive deal. The purchasers would pick up all the liabilities and contracts, (defined under the Agreement), plus a maximum sum of £571k, (which was dependent on any further player sales in the interim). Titley and Reeves also required, once an agreement about use of EP was concluded with Kennedy, to receive a £200k non-refundable deposit, (which would be counted towards the sale price). There’s always an argument to have this kind of arrangement – it deters chancers and tyre-kickers, but it certainly seemed steep to me.

..

That took us until mid-summer. The progress from thereon is catalogued in “In Administration – Part 2”

..

Next: In Administration – Part 2

Recent Comments